This post is sponsored by Lexington Law.

As we enter into December, most of us have the holidays on our mind. It’s easy to let it slip that the year is ending and we should start thinking about our money next year.

It can be overwhelming to start thinking about. It took me years to develop a system that allows me to have a grasp on my financial to-dos at the end of the year. And it’s still a work in progress as my life evolves and grows. For example, in 2019 I welcomed my first child into the world and that impacted my budget in ways I hadn’t predicted (I’ll share more on this in a post early next year).

Today I want to share with you a list of steps to take before the end of the year to start 2020 off on a high financial note. These are some things I recommend prioritizing for a fresh start in January.

10 Things To Do In December To Start 2020 Off On a High Note

1. Review your budget from last year and update it for next year.

Of course this was going to be first on my list. It’s hard to do anything with your money if you don’t know where it’s going, right?

Review how much you have coming in and where you spent it. If you don’t already use a tool like Mint, You Need a Budget or Personal Capital it might be a long process to do this by hand but having the exact figures will help you have a more clear vision of where your money is being spent.

After you’ve reviewed your budget for last year, it’s smart to make updates to your spending categories for the upcoming year. This way you’ll spend your money more efficiently. If there are categories you are overspending in, consider the reasons why you might be overspending there and brainstorm strategies to improve on that category.

Here are few posts we’ve shared on budgeting in the past:

- How To Budget To Improve Your Credit

- What To Do When You Get Your Paycheck

- How I Would Budget To Live on Less Than $10k/Year

- How to Create a Budget That Works With Your Spending Habits

2. Do an annual financial audit.

A few months back I shared a guide with a free checklist download on how to do an annual financial audit. Doing a financial audit is a very in-depth process. You’re getting up close and personal with your money.

I advise doing this process at least once a year. My husband and I always do it in December so that we can have a clear picture of how we did on our goals for the year.

Click here to read how to do an annual financial audit!

3. Update your debt repayment plan.

If you have debt, how is your progress going on paying it off? Are you on track or have you fallen behind?

It can be scary to have a huge number hanging over your head that you have to pay back. My debt at its highest was $25,000. And while that might be less than the average student loan debt in 2019 of $31,172, it’s still a large number.

Early on in my adult life I decided that I needed to prioritize paying it off. It took different sacrifices so that I could double and triple my payments. But the financial freedom I have now was worth it. I cried nearly every time I had to make a payment on my debt. I couldn’t wait for it to be gone.

If you’re not on track to pay off your debt or aren’t paying it off as aggressively as you would like, do some financial modeling to figure out a payment plan that helps you reach your payoff goals and also still enjoy your life with.

4. Set a goal for where you want to end next year with your finances.

One of my favorite parts of looking over my finances is picking goals for next year. Most of my goals are income and savings goals truth be told.

I always love reviewing what I achieved in the past year and devising a growth strategy for how to reach my goals next year.

Do I always hit them? No. But I usually get pretty close. And having these goals gives me something to work towards and strive for.

I also like to set other goals too like using up as many beauty products as I can or planning a big trip to celebrate my 30th birthday next summer.

5. Plan for a no-spend January.

A lot of us end December with a financial hangover of sorts. We’re all spent out from the holidays — figuratively, financially, and many times, quite literally too! A no-spend January is an excellent way to start the year. Erica from Coming Up Roses has an excellent guide on How To Do a No-Spend Challenge.

I’ve done no-spend Januarys and Februarys in past years. It’s interesting to start the year off with a challenge that keeps me from spending unnecessarily. During the holiday season we are often spending a lot of money and that can roll over into January and beyond if we’re not mindful.

6. Check your credit report.

Checking your credit report is one of those things you should be doing at least once per year but many people forget to do so.

It’s way too easy to put it off checking your credit report and waiting until later, but doing so could be a costly mistake. The holidays are prime time for identity theft. We’re using our credit cards a lot more frequently and often times at new places. This can make us vulnerable to having being a victim of a stolen identity.

You can get yours for free once a year at annualcreditreport.com. Go through line by line and make sure everything is correct. The primary things you are looking for are inaccuracies and unfair negative items.

If you do find either of these things on your credit report, I recommend reaching out to the credit repair professionals at Lexington Law for a free consultation. Your credit is a tool to help you achieve financial freedom. Your credit score and credit history have the ability to save you or cost you tens of thousands of dollars over the course of your lifetime. If something is incorrect, unsubstantiated or unfair on your credit report, it’s worth it to take action immediately.

After the initial consultation, if you then decide to move forward with Lexington Law’s credit repair service, you’ll pay $14.99 to pull your full credit reports from TransUnion, Equifax and Experian. You won’t be charged for additional services for five days afterwards.

Related: Credit Repair: Why It Matters With Lexington Law

7. Adjust your automatic savings transfers.

Like I said before, one of my goals is almost always to save more money next year than the year before. One way I do this is by upping my automatic savings transfers.

After mapping out all my expenses for this year from the previous year’s budget, I can see how much more I’m able to transfer.

Even if you can only increase the transfer amount by $5, that difference will still add up over time!

8. Make sure your emergency fund is up-to-date.

As our month-to-month expenses change over time, it’s easy to forget to update our emergency funds.

For example, now that there is a third member in our family, our monthly expenses are slightly higher than they used to be. We also purchased a car this year and now need to include our insurance premium in our emergency fund.

Once you’ve updated your budget, you’ll have a clear picture of exactly how much you spend every month. Then you can see what are fixed expenses, which are variable, and which are non-essential in case of loss of income. For example, I will still need to pay my rent but I won’t be buying any new clothes if our income suddenly changed.

I’ve created an entire guide on how to calculate what exactly needs to be in your emergency fund — check it out and bookmark it here.

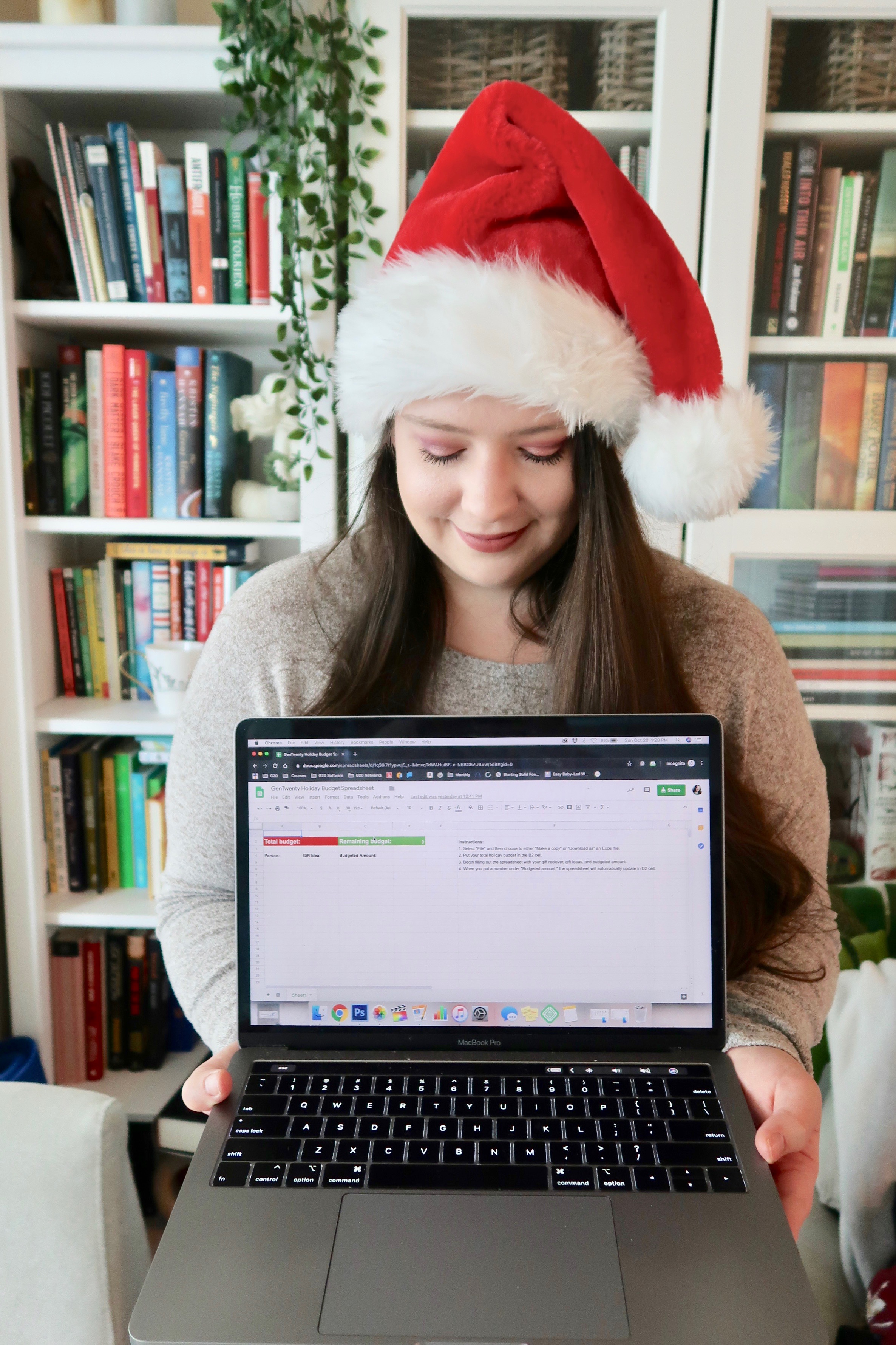

9. Make a spreadsheet for your holiday spending.

Our holiday spending can sometimes get out of control. I’ve found that making a spreadsheet (with tabs to separate the years) helps keep me organized when it comes to my holiday shopping.

I can set my total budget and track how much I’m spending on each person so that I don’t end up going over budget. You can set up the cells to automatically update the the budget you have remaining as you spend so that you don’t end up spending more than what you set for yourself.

I’ve also found that having the historical data (who I bought gifts for, the amount I spent, and what I bought) has been helpful to have year after year. Last year I spent about $1,900 on 30 people. This year I currently have 41 (!!!) people on my spreadsheet, so I know I’ll likely spend a little bit more than I did last year.

Here’s my guide on how I create my holiday spreadsheet every year. A free download is also included — no sign up or email required!

10. Negotiate a bill.

Wouldn’t it be great if you could reduce at least one of your fixed monthly payments? One thing I’ve learned is that it never hurts to ask!

If you have a list of your monthly fixed expenses (which you will if you update your budget!), start figuring out which one you’re most likely able to reduce. Your phone bill, cable bill, or an insurance bill are a likely bet. Star by comparing plans from other providers. Do they offer a better deal on the same service? That’s a great place to start with a negotiation! Companies want to keep you as a customer so oftentimes they’re willing to work with you on the price.

Either call the customer service line or even chat with them via a chat box on their website. Getting anything off of your bill is something I would consider a win!

As we enter a new year and a new decade, I hope you’re excited and looking forward to reaching new goals and bettering your finances. These are just 10 things you can do this December to start 2020 off on the right foot!

About the Author

Nicole Booz is the founder and Editor-in-Chief of GenTwenty, GenThirty, and The Capsule Collab. She has a Bachelor of Science in Psychology and is the author of The Kidult Handbook (Simon & Schuster May 2018). She currently lives in Pennsylvania with her husband and three sons. When she’s not reading or writing, she’s probably hiking, eating brunch, or planning her next great adventure.

Website: genthirty.com