This post is sponsored by Lexington Law.

Whether you’re trying to raise your credit score or just trying to keep your financial health on track, there are some lesser known credit facts that can make your life a whole lot easier.

Think of these credit facts as life hacks that make it easier to be financially confident.

5 Credit Facts That Work In Your Financial Favor

1. The debt-to-credit utilization ratio has a magic number.

One of the biggest factors that goes into your credit score is the debt-to-credit utilization ratio. In fact, this little number is weighted at 30% of your FICO credit score. Your utilization ratio is calculated by measuring your revolving balances against your total credit limit.

Let’s dig into this a little deeper. There are two types of credit utilization: line-item and aggregate. Line item is the ratio per line of credit. Aggregate is the ratio across all of your lines of credit.

Here’s an example of that in action:

Line item utilization (divide balance by the total limit):

1 Card Balance: $2,500/$10,000= 25% utilization

2 Card Balance: $5,000/$10,000= 50% utilization

3 Card Balance: $1,000/$10,000= 10% utilization

Aggregate utilization (divide your total balances over your total limit):

$8,500/$30,000 = 28% utilization

Both of these matter! In order to maximize this factor of the FICO credit score, aim to keep all of your credit cards below 30% utilization — AKA less than 30% of each card’s limit and less than 30% of your total available credit.

2. You can obtain your credit report for free once a year.

Thanks to the Fair Credit Reporting Act (FCRA), you can get a free copy of your credit report every 12 months. Being able to check your credit report for free gives you the opportunity to check for inaccuracies and fraudulent items on your credit report.

To get yours, go to AnnualCreditReport.com. Download a copy of all three of your reports and check them for incorrect information. You’ll also want to make sure all of the correct information is on there, too. Missing information that could potentially be beneficial for you shouldn’t be overlooked either.

Pro-tip: You can also purchase copies from each credit bureau (Equifax, Trans Union, and Experian) directly. Additionally, they’re often given free of charge when you’re enrolled in a credit monitoring service!

3. A good credit score will save you thousands of dollars across your lifetime.

Having good credit can save you thousands of dollars in interest payments. Not to mention you’ll have more freedom in what you choose for yourself in life.

A lack of credit can keep you from buying a home or taking out a car loan. A poor credit score means higher interest rates which in turn, means more money paid over time. Even a difference of a few percentage points in your interest rate can add up to tens of thousands. Here’s an example of the impact of damaged credit:

| CREDIT STATUS | RATE | PAYMENT | COST OF BAD CREDIT |

|---|---|---|---|

| Excellent | 3.9% | $1,179.17 | $0.00 |

| Mildly Damaged | 5.0% | $1,342.05 | $58,637 |

| Damaged | 6.3% | $1,547.43 | $132,574 |

If you feel like your credit score has room to improve, there are things you can do now to start to improve your score in the next six months. If you’re not feeling optimistic about your situation, I encourage you to reach out to the credit repair consultants at Lexington Law. In the world of credit repair, it’s so beneficial to have someone in your corner who not only knows the law but will advocate on your behalf.

4. Actively monitoring your credit can help you spot fraud.

While you can check your credit report for free once a year, signing up for a credit monitoring service can alert you much more quickly in the case of fraud. These services are able to check your credit report for changes much more frequently. Not only does that save you time from checking and comparing yourself, but you could potentially save thousands of dollars by spotting inaccurate items right away.

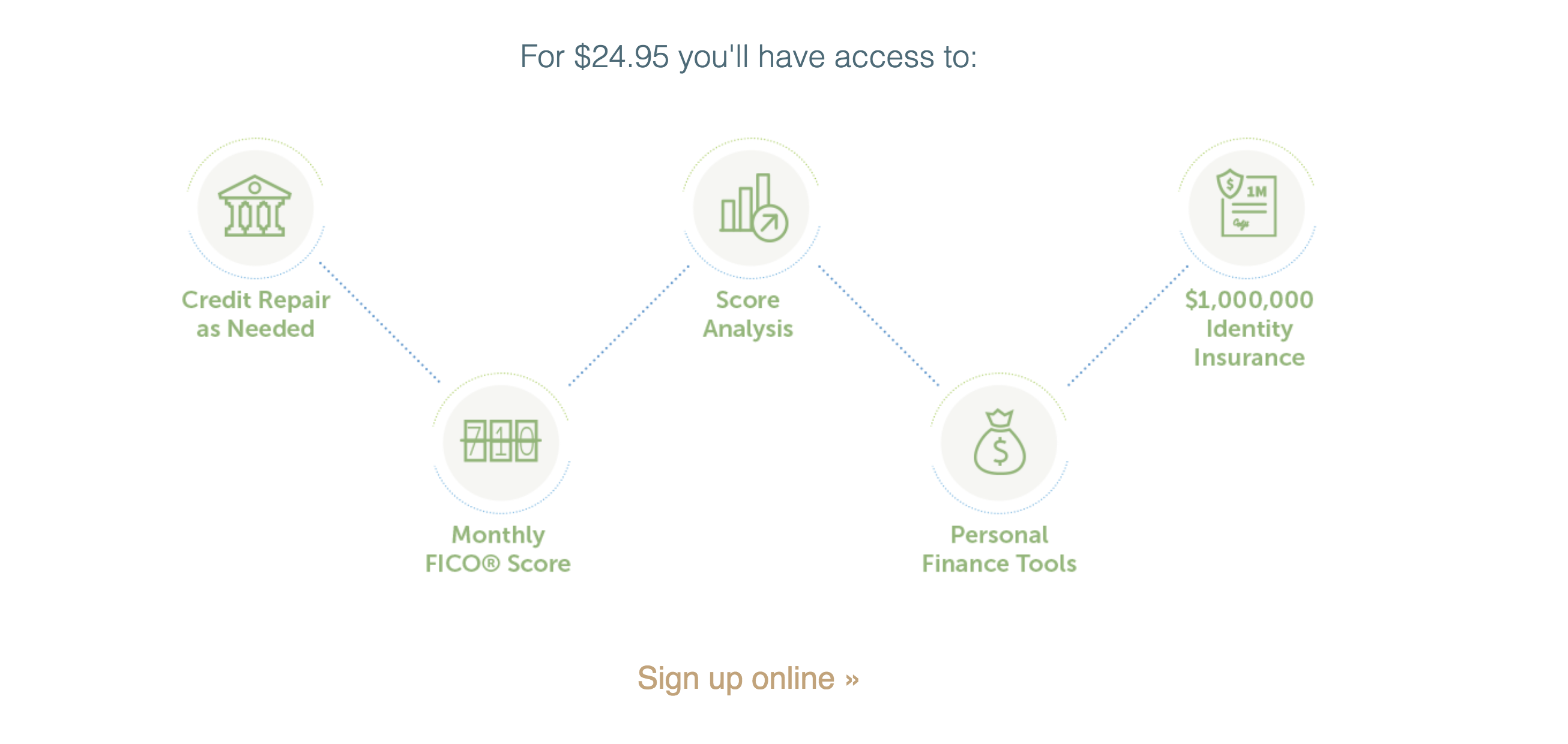

Using a service like Lex OnTrack will notify you of changes on your credit report on a monthly basis. You’ll also have access to your FICO score, as well as a credit score analysis that can give you insight into how to improve your score. Plus, you get credit repair on an as-needed basis, and $1,000,000 in identity insurance which is massively beneficial in the event of identity theft. It happened to me, and I learned my lesson — more on that in an upcoming post!

Actively monitoring your credit is one of the easiest financial; things you can do to protect your future self. Your credit report, score, and history is important, and it’s something you should be taking seriously.

5. Negative items can age off… but they can also be disputed and removed early.

You’ve probably heard that items age off of your credit report in seven years. While this is true, it’s not the whole truth. Some things, like bankruptcies for example, can stay on your report longer than seven years.

However, credit grantors and credit bureaus can actually remove those negative items from your report at any time.

As the credit repair consultants at Lexington Law explain,

Creditors want consumers to believe the lie because they can charge higher rates of interest to those who have nasties on their credit reports. As far as they are concerned, the longer the stuff remains on consumer credit reports collectively, the larger their profits. The truth, though, is that nobody is required to report anything about any of us for any minimum length of time to anybody else. Put bluntly, relevant laws like the Fair Credit Reporting Act only serve to place LIMITS upon how long items can remain on reports.

This works in your financial favor because those negative items on your credit report can be removed sooner than you thought. And you’ll be improving your credit along the way. I call that a win!

And there we have it! Five credit facts that work in your financial favor that can start making a difference in your life today.

About the Author

Nicole Booz is the founder and Editor-in-Chief of GenTwenty, GenThirty, and The Capsule Collab. She has a Bachelor of Science in Psychology and is the author of The Kidult Handbook (Simon & Schuster May 2018). She currently lives in Pennsylvania with her husband and three sons. When she’s not reading or writing, she’s probably hiking, eating brunch, or planning her next great adventure.

Website: genthirty.com