This post is sponsored by Lexington Law.

When people talk about the biggest money mistakes they ever made, it usually involves something along the lines of missing a one-off credit card payment or going over budget. While I’ve made money mistakes like these too, today I want to share mistakes that impacted my lifestyle and my values.

You see, here at GenTwenty, we believe that you should lead a savvy, value-driven life. You have goals and we want you to crush them. Your dreams matter and we want you to reach them. These money mistakes are ones that taught me extremely valuable lessons that I want to share with you.

The 4 Biggest Money Mistakes I’ve Ever Made (And What I Learned)

1. I moved into an apartment that was at the top of my budget.

When you start making your first real salary–you know the amount that you can live on your own with–it feels like the world opens up to you.

Post-college my husband and I moved across the country for his job. We had to find a new apartment in a new city where we only knew a few people. We made a quick trip out to get the lay of the land and do some research on neighborhoods and pricing.

After scoping out a few buildings that were lower in our price range, we had a tour of a building that a friend lived in. And instantly, to the dismay of our budget, loved it.

We had a very specific time frame that we had to move in which limited our choices to units available. Plus, it was summer. And as any leasing agent will tell you, it’s more expensive to start a lease in the summer months. We were mostly shown one bedrooms which were priced at the very top of our budget. After running the numbers, we ultimately decided to sign the lease. Since we loved the location and the amenities, it seemed worth it.

In the end, it both was and it wasn’t. Looking back, putting us at the top of our budget meant we had so little money for everything else. That meant less money for paying off debt, for saving, and for fun. We also couldn’t even afford to buy more than $1,500 worth of furniture at IKEA for over six months. Half of our apartment sat empty.

I regret not considering a smaller apartment. To the best of my memory, we didn’t even consider renting a studio which would have saved us close to $1,000/month. The space would have been perfect for us in our new city and given us more financial freedom. I’ve spoken previously about how after renting this apartment, we moved in with roommates for a year. That cut our costs by $900/month. And after that year was up? We spent three years living in a studio that was only 650 square feet. It was completely doable and our finances were significantly better off for it.

The lesson learned:

You probably need less space than you *think* you do. And on top of that, never buy or sign a lease on anything that is at the top of your budget. Whatever you estimate your budget to be, reduce it by 10-20%. Your bank account will thank you.

2. Not advocating for myself in the financial aid office.

When I graduated from college, my student loan debt was around the $25k mark. Of that $25k, nearly $18,000 of it came from my senior year alone.

I was lucky enough to earn grants and scholarships that funded most of my higher education. I also qualified for low-income family grants, work-study scholarships, and first-generation college student grants. While I had those funds, I also worked two jobs for two and a half years, and one job for the remaining year, to make up the difference. There is only one semester of college (my very first one) that I did not work and go to school full-time.

Generally freshman and sophomores are given priority for many of the higher grants. From my knowledge, this is to encourage kids to go to college and pursue higher education. Unfortunately for me, that meant I wasn’t granted this assistance to finish off my four-year program.

I took the required paperwork to the financial aid office. After a terrible mishap where I dropped the folder behind a heater and had to call maintenance to come get it out, I had a discussion with an advisor. They informed me there was nothing they could do and the money just wasn’t there to give me even though I qualified.

I left feeling defeated and did what I thought had to do to and took out loans to cover my tuition and expenses.

A few months later, I found out a girl I knew had gone through the same process I had but continued to persist. For months she went back and forth with them but eventually was granted the funds to cover her tuition.

The lesson learned:

You have to advocate for yourself. No matter what the situation is, you need to take action for your behalf. Don’t sit and wait and hope things will get better.

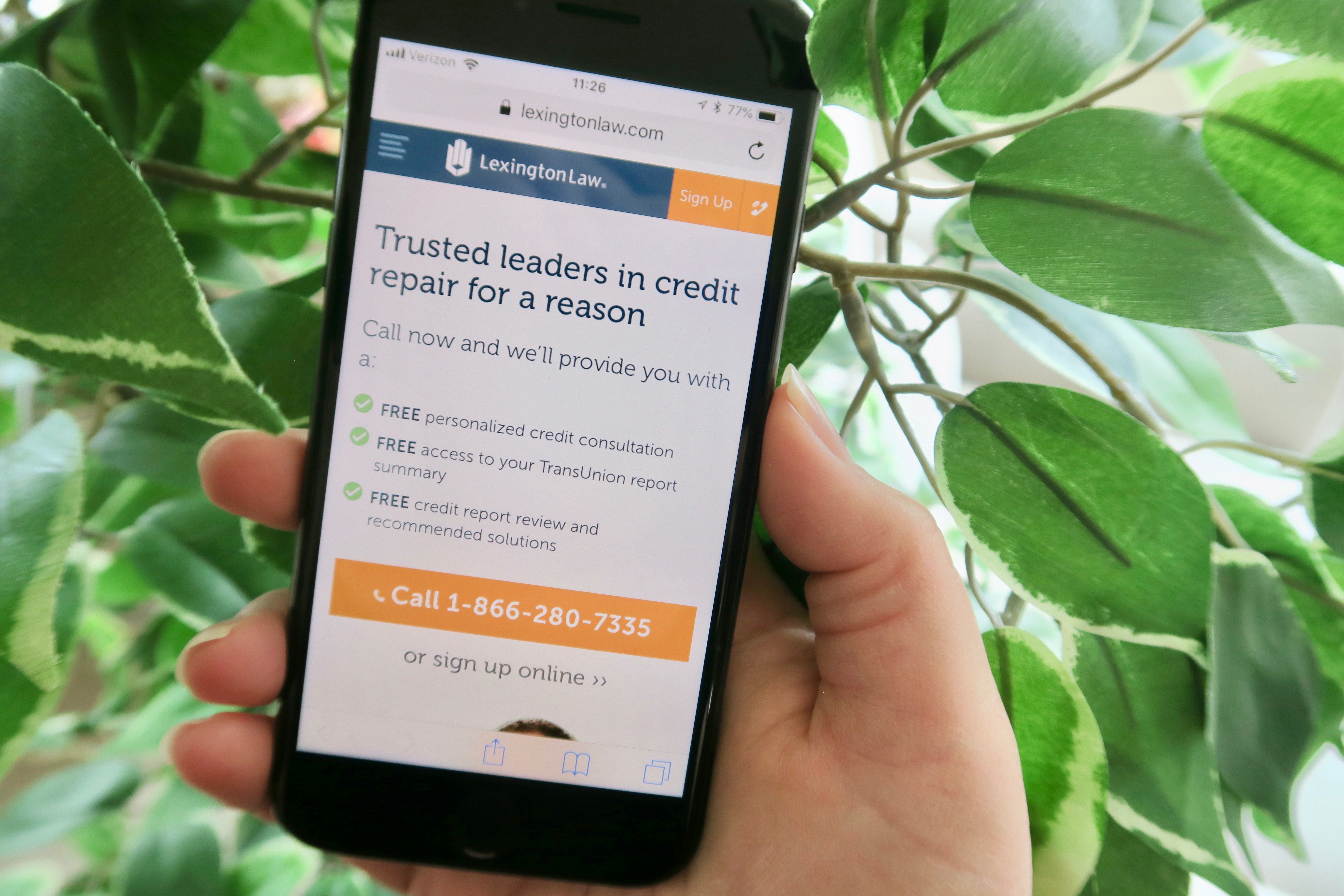

And reach out to resources when you need them. For example, you might find yourself struggling to understand your credit report or with a slew of inaccurate items (like in lesson #4). I recommend contacting the credit repair professionals at Lexington Law for a consultation. With intimate knowledge of your credit rights as a consumer, they advocate on your behalf and work on a game plan to resolve inaccurate items.

3. I didn’t buy the concert tickets.

This may seem weird, but let me explain. There’s been twice in my life where I wanted to go to a concert, but eventually decided not to.

The first one was Taylor Swift’s Speak Now Tour in August 2011. I was working my summer job at school and desperately wanted to go. I was trying to save money so instead of dropping $200+ on tickets, I lived vicariously through social media. As I’ve now seen every concert since then, and most of them twice, I still regret not going. I probably ended up spending that money on eating out and clothes I no longer own.

The second time was when Lorde played a tiny venue in my city in September 2013. Her music was very new at that point and I didn’t even know all of the words, but I wanted to go. I didn’t know anyone who wanted to go with me, so I decided not to. I ended up eating Mexican food a few blocks away while the show was happening with a group of people I no longer talk to. Tickets to that show were around $15 and yet, I still didn’t go.

The lesson learned:

Experiences matter. Spending money on experiences matters. Now, whenever there is a show or event I want to go to, I just buy the tickets. Truth be told, it’s not very often. Maybe three or four times a year, but it’s worth it every time.

4. I was careless with my personal information.

I didn’t realize it at the time, but at some point, I had left myself vulnerable to identity theft. While I was in high school at the time my identity was stolen, it can happen to anyone.

The only reason I discovered it happened to me was because I was going to college. At the time, I was filling out information for small student loans and financial aid. That was when I checked my credit report for the first time. Truthfully, I wasn’t sure there wasn’t going to be anything there because I didn’t have a credit card or loan. But something told me it was a good idea to take a look anyway.

Luckily I listened to that voice because I ended up discovering that I had been a victim of identity theft. Someone had been using my social security number to work at a grocery store. Clearing it up required filing a police report and a lot of phone calls, but it taught me the importance of monitoring your credit report.

I still can’t be sure how this information ended up in someone else’s hands. Whether it was me or someone else, it’s irresponsible to be careless with your personal information. Be extremely mindful of who you share it with and how you share it.

Plus, in today’s digital world, personal information is stolen all the time. Data breaches happen, and who knows what might happen to your personal information. It’s better to stay on top of it, in my opinion.

The lesson learned:

It can leave you feeling vulnerable when something that should be yours alone is taken from you. You need to protect your identity at all costs. This means keeping important documents in a safe, updating passwords frequently, shredding documents with personal information on them, and use an identity monitoring service.

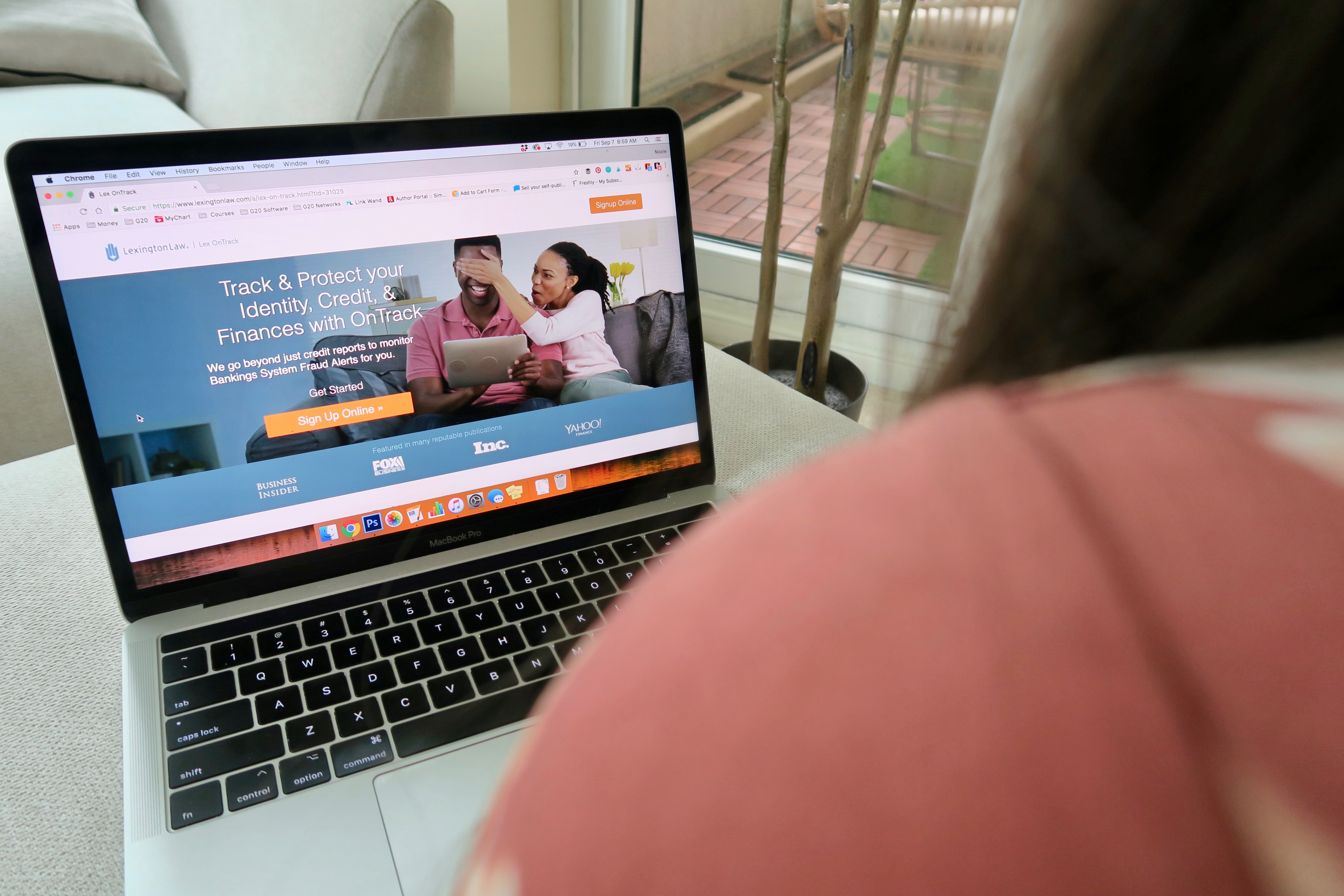

It’s really up to you to remain diligent. That situation is why I use a credit monitoring service, like Lexington Law’s OnTrack Tool, to monitor my identity on a daily basis. As we get older, the financial stakes are higher and situations can become stickier. It gives me peace of mind to know that I will be alerted of changes on my credit report. Other benefits of the tool include access to your monthly FICO score, credit score analysis, credit repair as needed, and $1,000,000 in identity insurance. For peace of mind, it’s worth it.

Those are four of the biggest money mistakes I’ve ever made. I don’t think making mistakes is necessarily a bad thing. Many of us need to learn firsthand the consequences of something before we truly understand the depth of the matter. I hope that with my experiences, you’ve learned something important that will help you change your habits.

Remember, spending more than you can afford to will put a strain on your whole life. You need to advocate for yourself, and if you can’t, contact someone who will. The experiences are worth the expense. And your personal information is valuable and needs to be protected.

Let me know below what the biggest money mistakes you’ve ever made are! And don’t forget to share what you learned as well.

About the Author

Nicole Booz is the founder and Editor-in-Chief of GenTwenty, GenThirty, and The Capsule Collab. She has a Bachelor of Science in Psychology and is the author of The Kidult Handbook (Simon & Schuster May 2018). She currently lives in Pennsylvania with her husband and three sons. When she’s not reading or writing, she’s probably hiking, eating brunch, or planning her next great adventure.

Website: genthirty.com