If you’re living paycheck to paycheck or simply don’t have a lot of wiggle room when it comes to luxuries, reeling in your spending can be a struggle.

Trust me, I feel your pain. When your friends are going out to eat and you want to go see everyone, or there’s a piece of furniture that you’re dying to have from Target and once you buy it your apartment will be perfect, but you just don’t have the money for it.

But that’s what credit cards are for, right?!

No.

And while I’ve had plenty of emergency expenses that have racked up my credit card debt (hello child custody lawyers), I have also done my fair share of overspending.

After I decided to consolidate my credit card debt with a much lower interest personal loan (boosting my credit score from 720 to 780), I knew that I needed to drastically cut down my spending to ensure there weren’t any tight moments where I’d have to pull my credit cards out in order to afford something that I really didn’t need.

That’s why I decided to create a money diary. I knew I needed something to keep myself accountable and to track my spending.

However, a money diary does more than just track spending. It helps you to plan out your expenses accordingly based on your weekly budget so that you know how much you have left for entertainment, Target trips, date nights, and more.

How To Use a Money Diary To Take Control of Your Finances

1. Create a weekly budget.

In order to get started creating a successful money diary and really have control over your spending is to know how much you’re able to spend each week.

After all, tracking your spending means nothing if you’re not doing anything to stop your bad spending habits. This is why you need to start your money diary journey by creating a weekly budget.

Personally, I use Clarity Money to manage my finances, and one of their most recent features allows you to set up a weekly budget based on your income versus the amount you spend on bills each month. It then breaks your leftover income down over weeks so that you know what you’re able to spend comfortably.

2. Map out your essential expenses.

When I create my budget, I calculate my income minus my monthly bills, like rent, car payment, insurance, loans, etc.

After I get my budget, then I start to look at some of my other expenses, like grocery shopping and gas. Since those are expenses that I’m not able to get around, they come out of my weekly budget first.

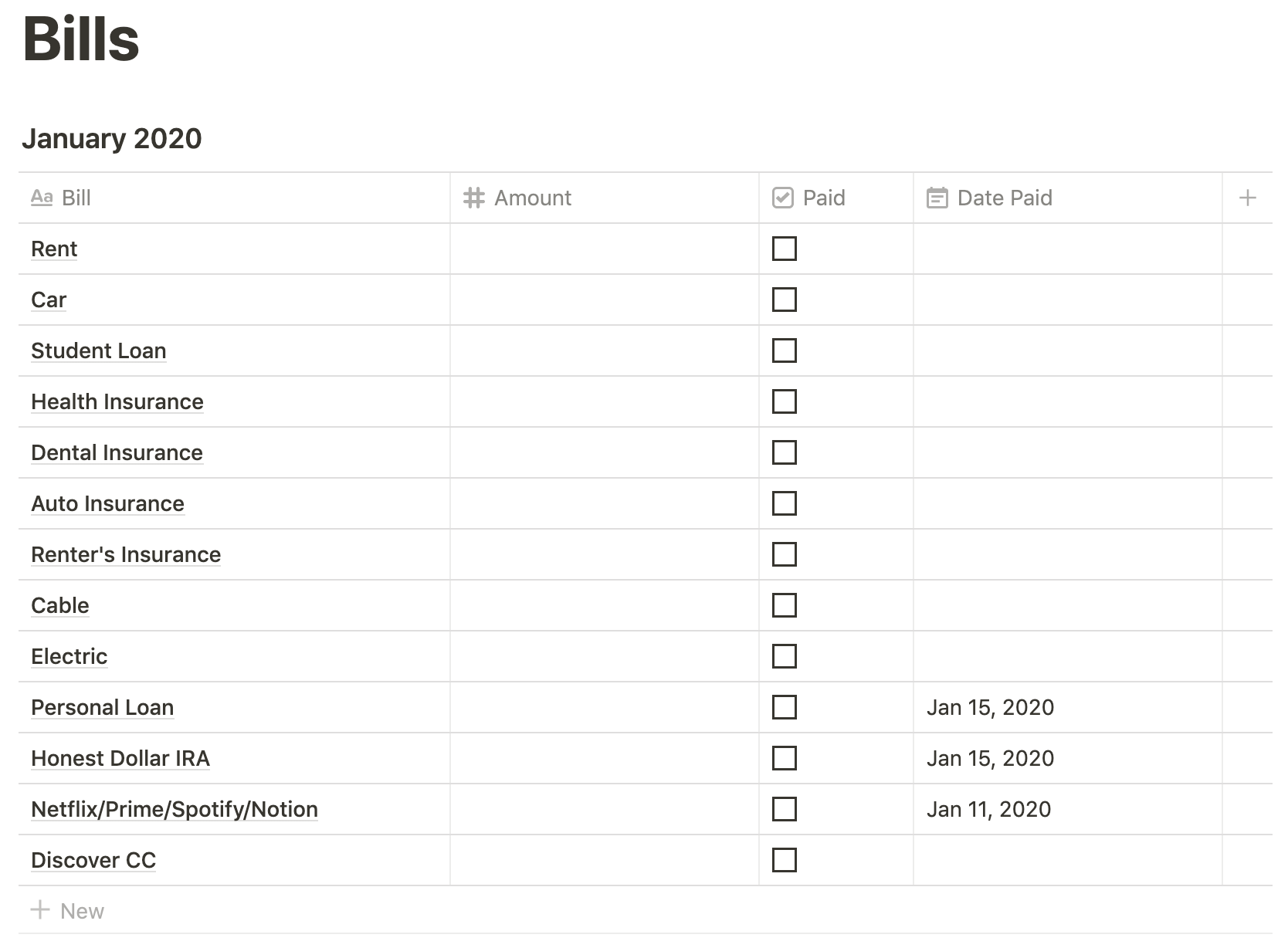

I’ve set up my money diary in my favorite project management tool Notion as a table with the days of the week in the first column, things I’ll have to pay for in the middle column, and money allotted for each day/item in the third column. Then I simply create a new table each week and start anew.

Other ways to implement a money diary:

You can also do this with a project management software, in an Excel spreadsheet, or in a bullet journal. Find a format that works for you and that makes you happy to use so that you’ll come back to it regularly.

Notion tables and Excel spreadsheets make it easy because you can have them add up your daily expenses and quickly find your weekly spending amounts to ensure they’re on par with your budget.

Based on my plans for the week, overall meal plan, and food I have left in my fridge/pantry, I’ll pinpoint which day I’ll need to do my grocery shopping. I allot myself $100 grocery budget each week. (Sometimes less if I have an expensive week or need fewer items.)

Next, I try to plan out which day I’ll need gas. When I was commuting to work each day, a tank lasted me almost exactly a week each time, making it easy to plan when I would need a refill. But now that I work from home and drive much less, planning the date I’ll need gas is sometimes a bit of a gamble.

There are other weeks that I’ll have more essential expenses, like my therapy copay, my wax appointment, and the like, but groceries and gas are my big ones.

Figure out which weekly expenses are non-negotiable and set a budget or allot a set amount of money that you can (or need to) spend on them.

[Tweet “How To Use a Money Diary To Take Control of Your Finances”]

3. Plan the rest of your week.

After you’ve added the essential expenses into your money diary, it’s time to plan out the rest of your week.

If you know of plans that will cost you money already (maybe you’ve got a date night planned or you’ll need to pick up a bottle of wine on the way to a movie night with friends), add those in first.

The next step is to determine how much money you can spend. If something has a set cost already, then you don’t have much flexibility and you have to add that to the Money Allotted column.

However, if it’s something like date night or dinner with friends, set a limit for yourself.

One of my worst habits is that when I go out to eat, I won’t pay attention to how much things cost and I’ll order multiple drinks, dessert if I want it, and maybe even hit up a cocktail joint afterwards.

The problem is, I have many weeks where I simply can’t afford to do this. I need to be intentional about my nights out. So I’ll set a reasonable budget based on what typical dinners out cost in Downtown Charleston plus a single glass of wine to drink and the tip, and that’s the money allotted for that day/event.

If you’ve planned out your week and you haven’t used up your full budget, you have two options – you can allow yourself another event or perhaps some personal shopping or self care, or you can move onto step number four.

4. Put the rest in savings or roll it over.

Ideally, you should be budgeting for your savings each week. But if you’re busy paying down debt or you’re living paycheck to paycheck, that’s not always an option.

This is important to remember: you don’t have to spend your full budget every week.

Just because you have some money left over doesn’t mean you need to find a way to squander it. Save it for later or roll it over if you know you have an expensive week coming up.

[Tweet “Budget tip: Just because you have some money left over doesn’t mean you need to find a way to squander it.”]

In the same vein, you don’t want to completely limit yourself from going out and enjoying luxuries or dinners out in order to save money. You’ll get burned out and frustrated quickly, and if you’re anything like me, you’ll binge spend and completely lose track of your spending all over again.

Save when you can, put that extra money towards a higher credit card payment next month, or roll it over to a more expensive week.

5. Get your friends and family on board.

I love going out and doing things with friends and family. As I work from home, and at the end of many days, I want to get out of my home.

I also am terrible at saying no. Even if I know that I can’t afford something, if a friend is like “Hey, let’s grab lunch!” I’m notorious for doing it anyways and just charging it on a credit card.

This has been a terrible habit and it’s something that I’ve had to stop.

In order to help work on this, I’ve let my close friends and family members know that I’m putting myself on a strict budget and only have a certain amount to spend each week, and that a random lunch out simply isn’t something I can do right now.

And while it can feel embarrassing having to tell friends that you can’t afford to do something, I’ve been surprised at the number of my friends that have been struggling with the exact same issues.

So things we’ll do instead include:

- Hosting movie nights with rotating hosts

- Cooking at home and inviting friends over

- Having game nights with BYOB and BYOS (snacks)

- Taking advantage of free or cheap community events

(Stopping by the grocery store for a bottle of wine and a veggie tray is much cheaper than an entire dinner and drinks out.)

Opening up to those close to you that going out to eat or having a big night out isn’t in the budget can help everyone involved to find more cost effective ways to get together.

What do you think about creating a money diary? Is this something that can help you to take control of your expenses?

Everyone’s financial management works differently, and finding a process that helps you to methodically plan out your spending and ensure you’re not going over budget is important.

About the Author

Chloe graduated from College of Charleston with a BA in English. She is currently a Content Marketing Manager at Visme and freelance writer. She loves brunch, stand up comedy, and card games. She works from home and plans to do so for the rest of her life.

Website: chloesocial.com