This post is sponsored by Lexington Law.

Whether you’ve just blown out the candles on your 20th birthday or you’re just a few years from the big 3-0, now is the perfect time to get your financial life in line with your goals. So where do you start? Don’t worry, you’ve got our ultimate financial checklist for your 20s to keep you on track!

Together we cover what you’ll want to accomplish throughout your twenty-something decade, what to do annually, what to check in on monthly, and brief weekly to-dos to keep you on track.

Now, I want you to keep in mind that this financial checklist is ultimately a framework to live by. You need to set your exact goals to get the most out of your 20s. For example, if you’ve already bought a house, you may be working on saving up for a second property. Keep this in mind as you go through the checklist!

We’ve also made a workbook that’s FREE to download to help you plan your way through your financial checklist. Get it here:

The Ultimate Financial Checklist For Your 20s

Overarching Goals for Your Financial Checklist

The timeline of these goals will vary throughout your 20s depending where you start and where you intend to end up. Keep them in mind as you set your annual financial goals each year!

- Pay off all of your debt. This should be one of the first things on your financial to-do list. Student loan debt and your consumer credit card debt should be completely (or nearly) eliminated by the time you turn 30. When paying off debt, consider how aggressive you should be based on interest rates and tax breaks when establishing your plan. There is both good and bad debt, and they can be used to your advantage!

- Save 6 months of expenses in an emergency fund. Loss of income can happen at any time. To avoid a financial disaster, get yourself prepared with a fully funded emergency fund. The amount you may need in an emergency fund will likely change throughout your twenties, so revisit this goal annually.

- Sign up for identity monitoring: With data breaches happening frequently, it’s up to you to make sure your identity and information is safe. There’s never too early of a time to sign up for this! My identity was stolen in high school. I’ve also personally been impacted by data breaches at various companies and even my university. Protect yourself with Lex OnTrack to be notified of changes on your credit report. You’ll have access to your monthly FICO score, score analysis, credit repair as needed, and $1,000,000 in identity insurance. It’s an investment worth making.

Growth goals to strive towards:

- Get your credit score in the excellent range. There are many benefits to having a high credit score. Three that our friends at Lexington Law point out include low interest rates and better lines of credit, your potential employment, and lower auto premiums. To get started, here are 4 Ways To Start Improving Your Credit Score in the Next 6 Months. If you have unfair negative items on your credit report, reach out to the credit repair specialists at Lexington Law to learn more about the options you have for credit repair. They’ll advocate on your behalf and make a plan that is right for your credit goals.

- Start investing outside of tax advantage accounts. After contributing to your tax advantage accounts, it’s time to start exploring other avenues of investing. To figure out where to start, here is our guide to Investing 101: A Beginner’s Guide to Investing For Wealth.

- Have multiple streams of income. Like diversifying your investments, diversifying your income streams can give you more financial security. Consider what side hustles can generate more income for you and what passive income streams might also work for you.

- Set a net worth goal that seems out of reach. The average net worth by age 30 is generally suggested to be somewhere around $90,000 – $100,000. What seems like an appropriate goal for you given your current net worth? Add $20k to that number.

- Seek help when you need it. Whether it’s credit repair or learning about types of investments or principles of advanced personal finance, don’t be afraid to seek out help when you need it.

[click_to_tweet tweet=”The Ultimate Financial Checklist For Your 20s with a FREE download!” quote=”The Ultimate Financial Checklist For Your 20s with a FREE download!”]

Annually

These goals should be visited annually. Set aside a weekend every January to make the needed adjustments.

- Review your financial goals for the year. It’s okay if your goals change. That’s why it’s so important to check in on them every year. As you get close to goals and check some off your list, set new ones! Here is our list of 5 Financial Goals To Achieve By Age 30.

- Update your automatic savings goals. As your financial goals for the year are adjusted and completed, you’ll need to adjust your savings for other goals.

- Check your credit report. You are entitled to a free credit report from each of the three major credit bureaus (Experian, Trans Union, and Equifax) every 12 months. To get yours, go to annualcreditreport.com. Go line by line to make sure your credit report is accurate and does not contain errors. Approximately 79% of credit reports do so be extra vigilant. If something is amiss, reach out to credit repair specialists to begin finding a solution.

- Get your credit score. Your bank or credit card may provide you with this information, however, you can also get your credit score for free here. Knowing this information will help you determine where you want to be a year from now.

- Make your budget. Reviewing your spending for the past year, what budget adjustments do you need to make? If this is the year you are going to double down and pay off your student loans, where is that money coming from. Did you rent go up? Adjust your budget to reflect that.

- Compare your net worth. Compare last year’s net worth to your current net worth. How far do you have to go to reach your goal?

Growth goals:

- Negotiate a raise. In order to make more money, you have to ask for it. Check out our guide to asking for a raise and promotion here.

- Adjust your 401(k) or Roth IRA contributions. In they very, very least, you should be contributing what your employer matches. To do the most, max out your contributions to the accounts. Your tax advantage accounts are your first step to retirement — and you should be taking advantage of them!

- Adjust your automatic monthly transfers. If you’re making more money this year, don’t use that money to upgrade your lifestyle! Put that money directly into your savings and investment accounts.

- Revisit your investment strategy. Look at your life milestones: Are you ready to begin investing for your child’s education? Are you done paying for your wedding? Have you funded your emergency fund? Adjust how your investment strategy for the year by aligning them with your goals and life milestones.

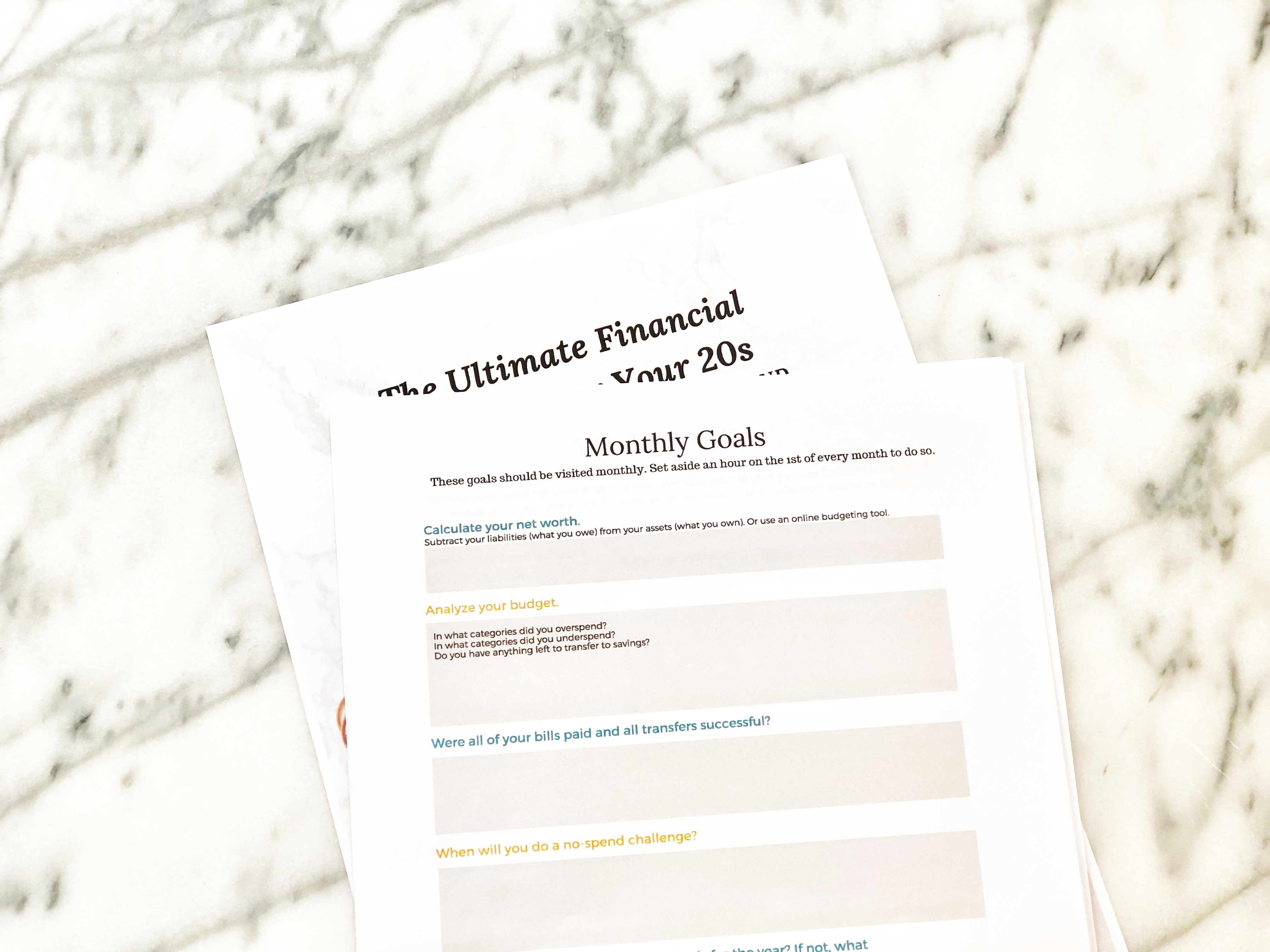

Monthly

On the first of every month…

- Calculate your net worth. You can do this manually by subtracting your liabilities (what you owe) from your assets (what you own). If you use an online budgeting tool, this is often calculated for you.

- Analyze your monthly spending and adjust your budget. Looking back over the month, what was your biggest budget buster? Did you eat out too frequently? Overspend on travel? Did sidewalk sales get you? Whatever your financial trigger is, find a solution for cutting back.

- Double check that all of your bills were paid and transfers went through. This should only take a few minutes max. Take a quick look at your accounts to verify everything was paid on time.

- Decide what to do with extra money. Did you make a little extra money this month from your side hustle? Sell some old furniture on a resale website? Decide what account you’re going to put that money into.

Every now and then…

- Do a no-spend challenge. I like to do this at least once a year. It reminds me that no, I don’t *really* need another lipstick and I can get by perfectly fine without a daily trip to Starbucks.

- Reaffirm you’re on target for your goals. Keep yourself in-line and make sure you’re on track to hit the financial goals you’ve set out to reach by the end of the year.

Weekly

Take a few moments every week to feel connected to your money by…

- Looking at your bank account. Make sure everything is in order and your spending is where it should be.

- Looking at your credit card statements. Double check nothing fishy is going on.

Having financial systems in place based on your goals simplifies your life. You know what you can spend based on your fixed expenses and savings goals. And, you’re making better decisions to pursue financial freedom.

So there we have it! The Ultimate Financial Checklist For Your 20s. You’re doing a wonderful thing for yourself by taking charge of your financial goals. When you set goals, budget, pay off debt, save for retirement and invest — your future self thanks you.

About the Author

Nicole Booz is the founder and Editor-in-Chief of GenTwenty, GenThirty, and The Capsule Collab. She has a Bachelor of Science in Psychology and is the author of The Kidult Handbook (Simon & Schuster May 2018). She currently lives in Pennsylvania with her husband and two sons. When she’s not reading or writing, she’s probably hiking, eating brunch, or planning her next great adventure.

Website: genthirty.com