This post is sponsored by Lexington Law.

Welcome back to Adulting and Money! Last week we discussed how to talk about money with your partner. This week, our topic is preparing your finances for a family — including adoption!

Adding new members to your family increases your household spending. There are many financial aspects to consider as you enter parenthood, many which are often overlooked. Here, we’re going to discuss financial housekeeping before the baby arrives, budgeting, unexpected expenses, and insurance. Let’s dive in!

Related: How I Prepared My Finances For a Baby

How To Prepare Your Finances For a Family: Financial Housekeeping

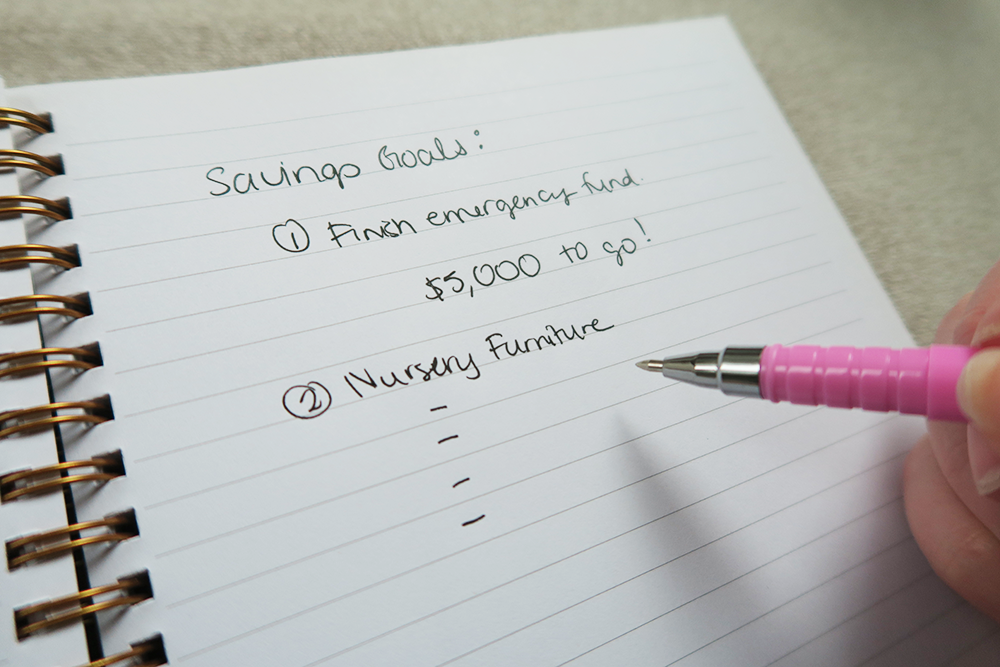

First things first, start saving!

You’re probably saving some money already, but if you’re not, it’s time! Growing your family can be a pricey endeavor — try this quiz and see how you do when it comes to care costs for a child!

Look at your budget and savings. If you’re saving for things like travel or new bedroom furniture, those things may need to take a backseat to your new addition. Begin directing that money into your aptly named “baby savings account.”

According to a 2010 USDA report, parents will spend around $12,000 during their child’s first year of life. This is a good starting number to aim for to get into your savings account before the baby is due. You can use some tips from building your emergency fund to work on reaching this number!

If you’re not currently expecting but hope to start a family in the near future, start saving a small amount from each paycheck for this purpose. If you’re currently expecting and have less than nine months to go, I recommend making this a priority!

Managing Your Debt

If you have debt I do think that you should prioritize both debt repayment and savings. With such a significant change in your finances approaching, your debt will also play a major role. If you’re taking maternity or paternity leave, make sure to factor in your potentially reduced income during that time. Check your company’s policy to learn what’s covered.

Make a plan for debt repayment as quickly as possible which still saving what you need. You’ll have to run through your own budget (covered more below) to determine what savings and repayment rates will be best for you.

Debt consolidation may or may not be the right choice for you. Check here to find out if it might be something worth consider.

Your Credit

When you’re expecting a new addition to the family, that might also mean moving to a new home or apartment and/or purchasing a new (or new-to-you) vehicle. If this is the case for you, realize that your credit score will play a major role in your financing on these big ticket items. Generally speaking, the better your score, the better your interest rate will be which means you’ll pay less over time.

Also take for example adoption. If you choose to adopt, fees can be exorbitant. The average adoption costs around $28,000. But that’s just an average. Many can exceed $40,000. If you don’t have this cash on hand, you may need to take out a loan. This will likely end up being a personal loan with a high interest rate — not ideal at this happy time.

Having excellent credit can be a way to help mitigate that interest rate (next to having a healthy savings account). Here are some ways to get your score up. If your situation is much more complicated, take it to an expert at Lexington Law who will walk you through your credit, make a detailed plan, and advocate on your behalf for removing negative items from your credit report.

Your Will and Estate Planning

Now that your family is growing, it’s important to have a will to establish what will happen to your child, your wealth, and your belongings in the event of your untimely demise. Make an appointment with a financial advisor and tackle these things early on.

You should also make sure you have life insurance. Whether you are a single income household or a dual income household, it could send them into financial turmoil to leave them with lost income. This is also a time to talk to your partner and make a financial plan should either of you pass.

Make Sure You’re Saving For Retirement

I strongly caution against forgoing retirement savings. You are in your prime earning years which means your money has time to grow in tax-advantage retirement accounts. As you age, your finances will need to be in order to avoid become a financial burden in the future.

Budgets, Health Insurance, and Savings

Pre-baby budget.

Though there might not be many things you feel the need to purchase right away, now is a good time to overhaul your budget and trim your spending.

Also start making a list of things you’ll need to buy in the coming months. This will be handy for making your baby registry as your due date approaches. Plus, it will also give you an idea of the big ticket items you need to save for!

During pregnancy, there are additional expenses for you as parents that you need to consider such as:

- Chiropractic care or prenatal massage

- Genetic testing

- Additional test that may not be covered by your insurance

- Purchasing a new vehicle

- Moving to a bigger space

- Maternity photos

It’s also a worthwhile idea to save for things that don’t get purchased from your baby registry that you’ll end up needing.

Post-baby budget.

There are going to be major differences in your pre and post baby budget. Generally your expenses will increase as your child gets older. This is why it’s important to be in the habit of saving early on!

You’ll also need to consider the added cost of a baby. As stated above, the average cost of an infant is $12k/year or approximately $1k/month. Mitigate this in ways you can like asking for gift cards on your registry to purchase formula or diapers post-baby. Shop for baby clothes at thrift stores and allow your child’s toy and book collection to be built up over time by well-meaning family members. Infants and toddlers grow very quickly meaning there is a fast turnaround in their needs during their first years of life.

Below, we’re going to discuss maternity and paternity leave as well as health insurance so make sure to factor those aspects into your budget as well.

Maternity/Paternity Leave

If you are planning to take time off after your child is born (which you absolutely should!), make sure you are informed of your company’s maternity/paternity leave policy. Sit down with an HR rep to make sure you understand it fully.

Some companies offer full benefits while you’re out of the office, others offer reduced pay, and others may offer none at all. The length of leave available may also differ so if you have questions — ask!

If you’re self-employed, you most likely can fund your own maternity/paternity leave through Short Term Disability Insurance. The biggest catch is that you have to have coverage before you become pregnant. Make sure to thoroughly read the policy so you know what you’ll be getting.

[Tweet “Adulting and Money: How To Prepare Your Finances For a Family”]

Health Insurance

After your baby is born, you’ll need to add them to your health insurance policy. If you and your partner both have the option, compare and contrast your health plans. One may be much better than the other in terms of cost and coverage. There may also be a window of 30-60 days for when you can add your baby to your coverage — make sure you know these dates and get all of your papers in line ahead of time.

You may or may not also want to purchase life insurance for your child. There are pros and cons for each side of the argument, but when it comes down to it, it depends on what is best for your family and your finances.

Saving For Baby’s Future

At some point, you’ll need to consider how you want to save for baby’s future. An Education Savings Account (ESA) is a good choice. You can add up to $2k/a year after taxes — the good news is that it will continue to grow tax-free. A 529 plan is also an option but opt for a flexible plan and be very mindful of restrictions.

You can also save money in a non-tax advantaged account to put towards things like piano lessons or private school as your child ages. Having that money in savings ahead of time will put less strain on your finances in the future.

Identity and Credit Monitoring

I don’t think there is a wrong time to sign up for identity and credit monitoring, but now is as good as a time as ever! Between feeding session and nap times, it’s going to be more challenging to track your everyday life, not to mention your finances. A service like Lex OnTrack can give you peace of mind while you focus on your newborn. Click here to learn more and sign up.

Adoption

If you are choosing to adopt, it’s still important to consider everything listed above! That said, adoption does come with some unique financial aspects to consider.

Funding adoption:

- Save: Most importantly, now is the time to begin saving if you are considering adoption in the near future. A healthy savings account and minimal debt shows you are financially responsible and prepared to adopt a child.

- Loans: Aside from saving, this is the most obvious way to get the funding you’ll need. As stated above, a high credit score can help immensely with keeping interest rates low.

- Grants: Depending on what you’re involved in locally, there may be grants available for you to put towards adoption. Check with your religious institution, community center, etc. or do a Google search to see what might be available in your area.

- Crowdfunding: A more unique perspective, it’s happening more and more frequently! Couples are being very open about their journeys to adoption and asking others to contribute. You could ask people to donate or fundraise in other ways such as offering your services like writing, consulting, yard care, babysitting, etc. You could also fundraise by partnering with local restaurants and retailers much like schools do.

Additionally…

- Talk to an adoption or family lawyer: You’ll want to make sure your bases are covered and your application is strong before investing time and money. Work with someone who knows what they are doing to get your application completed correctly the first time. The process looks into all aspects of your life to ensure you are a good fit for adoption.

- Clean up your credit reports: Now is a good time to also check your credit report for any incorrect information. Removal might take a few months to complete so the sooner you can get started on this, the better. Talk with an expert who will advocate on your behalf when necessary.

- Talk to a financial advisor: Your finances need to be in order as well before you begin the adoption application process. They can give you an idea of where you stand. There are also tax advantages to adopting, so you’ll want to know those too.

Whether you are planning to grow your family through either your own pregnancy or adoption, congratulations! This is a wonderful and exciting time in your life. It’s never too late or too soon to begin working on any of these financial aspects. Good luck!

Read the full Adulting and Money series here:

- How To Manage Your First Salary and Benefits

- Building Your Emergency Fund & Preparing Your Financial Future

- How To Talk To Your Partner About Money

- How To Prepare Your Finances For a Family

About the Author

Nicole Booz is the founder and Editor-in-Chief of GenTwenty, GenThirty, and The Capsule Collab. She has a Bachelor of Science in Psychology and is the author of The Kidult Handbook (Simon & Schuster May 2018). She currently lives in Pennsylvania with her husband and two sons. When she’s not reading or writing, she’s probably hiking, eating brunch, or planning her next great adventure.

Website: genthirty.com